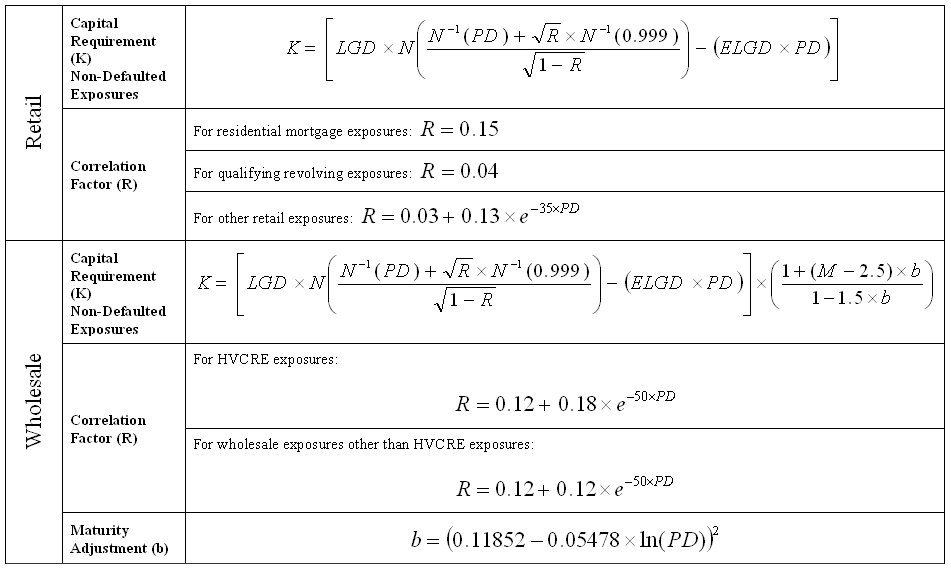

Definition Of Risk Weighted Assets Basel Iii

Risk Weighted Asset Definition Formula How To Calculate

Capital And Rwa For European Banks

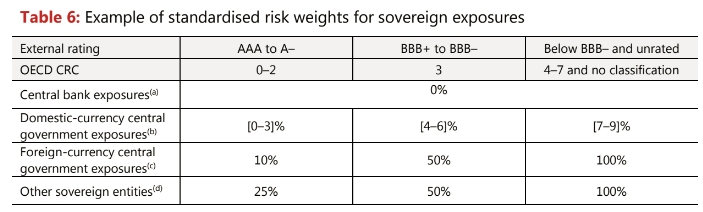

Risk Weights By Category Of On Balance Sheet Assets Download Table

Determinants Of Returns Do Risk Weighted Assets Affect Stock Returns Download Table

Impact Of Basel I Basel Ii And Basel Iii On Letters Of Credit And Trade Finance

Basel Iii The Impact Of Sovereign Risk Debts On Banks And Ecas Fv Txf News

This sort of asset calculation is used in determining the capital requirement or capital adequacy ratio car for a financial institution.

Definition of risk weighted assets basel iii. As per the basel committee on banking. Ensures that banks and financial institutions have a minimum capital maintained to be safe during times of uncertainty. The risk weighted asset can be calculated as below. Risk weighted asset also referred to as rwa is a bank s assets or off balance sheet exposures weighted according to risk.

Basel iii a set of international banking regulations sets the guidelines around risk weighted assets. Maintaining a minimum amount of capital helps to mitigate the risks. Risk weighted assets is a banking term that refers to an asset classification system that is used to determine the minimum capital that banks should keep as a reserve to reduce the risk of insolvency. In the basel i accord published by the basel committee on banking supervision the committee explains why using a risk weight.

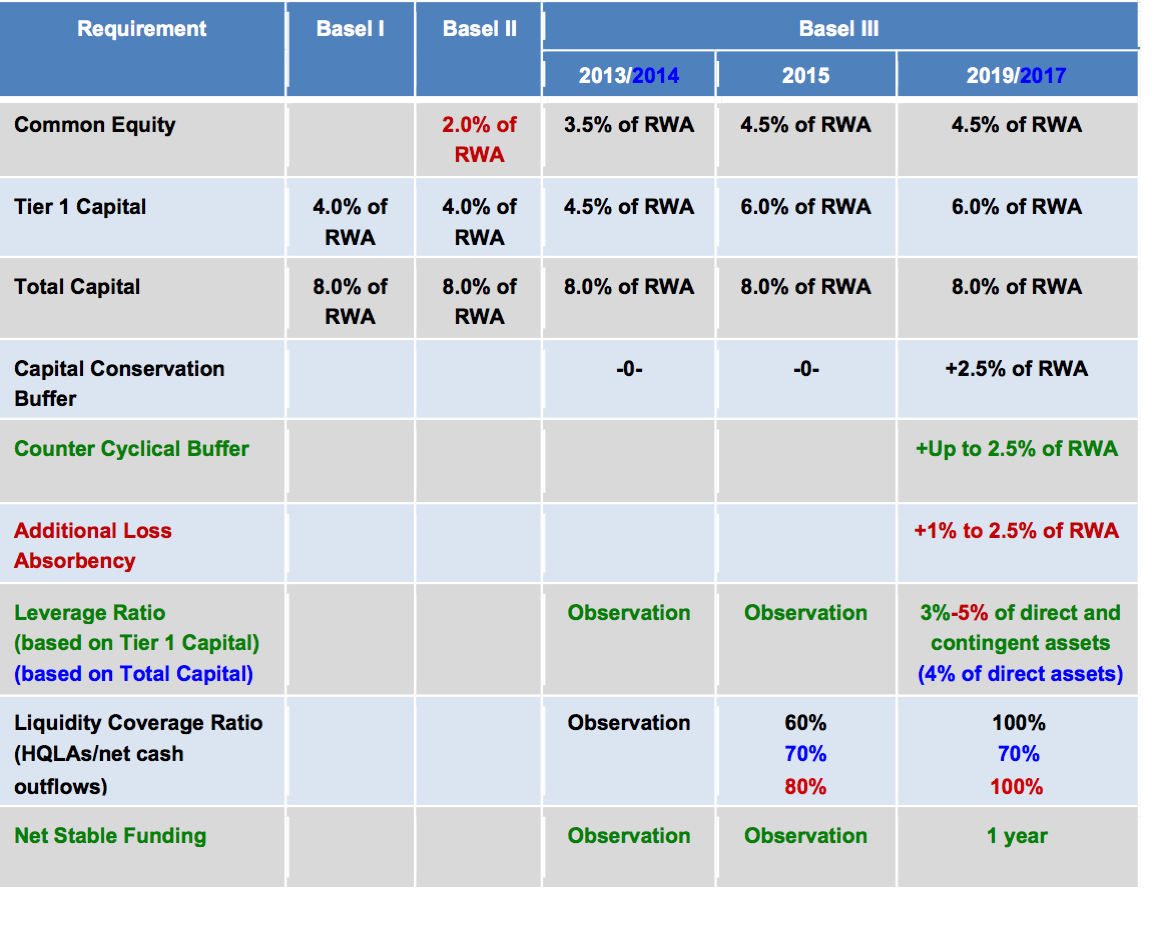

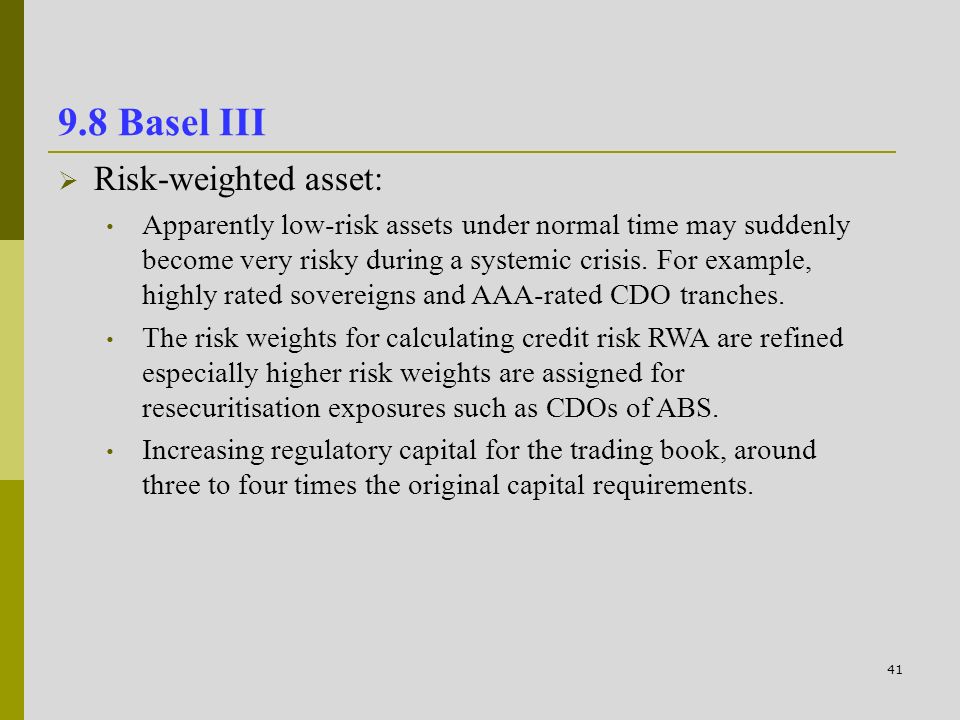

Basel iii increased common equity tier 1 capital from 4 to 4 5 of risk weighted assets rwas and minimum tier 1 capital from 4 to 6 compared to basel ii.

Definition Of Capital In Basel Iii Executive Summary

What Is Risk Weighted Asset What Does Risk Weighted Asset Mean Bankers Choice Youtube

What Is Risk Weighted Asset What Does Risk Weighted Asset Mean Risk Weighted Asset Meaning Youtube

Topic 9 Bank Regulation And Basel Ppt Video Online Download

Bank Risk Weights Under Basel Are Not Comparable Vox Cepr Policy Portal

Basel Iii What Is Basel Ii And Iii And What Does It Mean For Altfi

Basel Ii Capital Accord Notice Of Proposed Rulemaking Npr Preamble Calculation Of Risk Weighted Assets

7 Lower Percentile Estimates For Return On Risk Weighted Assets Rorwa Download Table

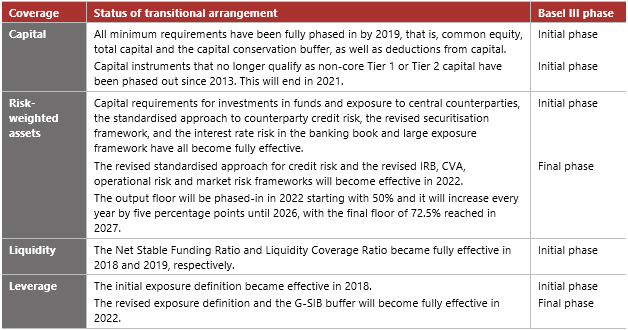

Implementation Of Basel Iii Executive Summary

Risk Weighted Assets Definition

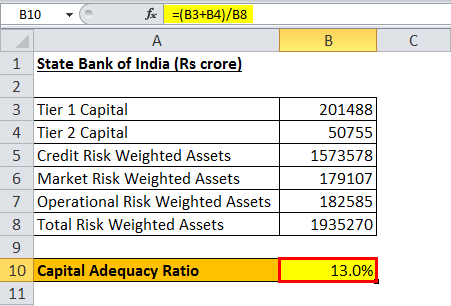

Capital Adequacy Ratio Definition Formula How To Calculate

Classification Of Risk Weighted Assets Banking Study Material Notes

Fdic Fil 86 2006 Proposed Rule On Risk Based Capital Standards Advanced Capital Adequacy Framework